After a strong first half of the year, technology stocks have come under pressure recently. Recent stock price trends suggest investors are taking a more cautious stance on the economy, while the surrounding frenzy Artificial Intelligence (AI) It has also been alleviated. Even the ones flying high Nvidia The stock has been affected, falling nearly 20% over the past six months.

But this sale also presents several opportunities.

Let’s take a look at three tech stocks (excluding Nvidia) that investors should consider buying amid this market correction.

1. Taiwan Semiconductor Manufacturing

Taiwan Semiconductor Manufacturing (NYSE: TSM)Or for short, TSMC is the world’s leading semiconductor manufacturing contract manufacturer. Today, many semiconductor company It doesn’t manufacture its own chips. Instead, it outsources the process to companies that specialize in chip manufacturing.

Outsourcing manufacturing may not sound like an exciting business, but don’t be fooled. It is a very complex process that is dominated by companies that can do it best. In fact, contract manufacturing units IntelFounded in 2021 to compete with TSMC, the chip designer has suffered a major setback recently. Broadcom Intel said its tests showed that its latest process is not suitable for mass production.

At the same time, TSMC has been leading the way in technological innovation, and the company plans to introduce 2nm production technology next year. The smaller the chip density, the better the performance and power consumption. As demand for AI chips continues to grow, the company has been increasing capacity and building new manufacturing facilities.

TSMC will also raise prices for advanced technologies as demand for its services grows. Morgan Stanley Analysts estimate that AI semiconductors and CoWoS (Chip-on-Wafer-on-Substrate) prices will rise 10% this year, high-performance computing prices will rise 6%, and smartphone prices will rise 3%.

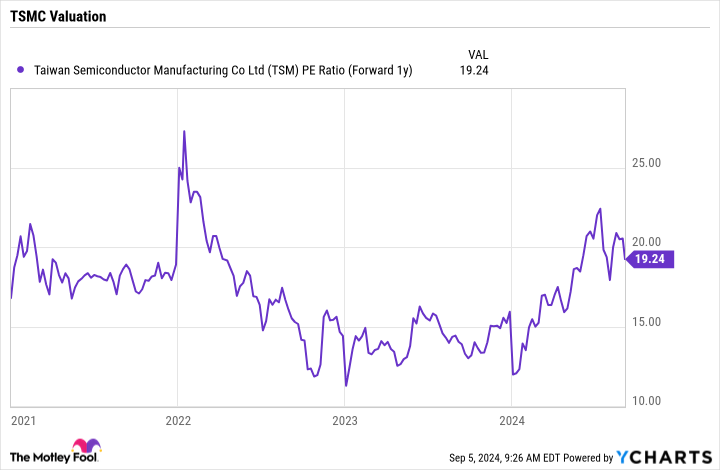

Trading at a forward price-to-earnings (P/E) ratio of around 19 according to analyst estimates for next year, the stock still appears attractively valued, especially given its growth prospects going forward.

2. ASML

TSMC produces chips for semiconductor companies, but korean: (NASDAQ: ASML) Companies like TSMC make the highly specialized equipment that is used to manufacture these chips. As TSMC and other companies expand production to meet the growing demand for AI chips, they will need more equipment to produce these chips.

Unsurprisingly, the semiconductor equipment manufacturing business can be bumpy because the equipment is very expensive. These machines typically have a life cycle of about seven years before they need to be replaced or repaired.

Meanwhile, 2024 will be a pivotal year for ASML as it launches its latest technology, A. High-NA EUV, or high-aperture extreme ultraviolet lithography system. The company says the new machine will increase chip manufacturing productivity while lowering production costs and improving chip functionality.

The company has shipped two high-NA EUV systems so far, one of which is now running qualification wafers. At $380 million per unit, the new system is expensive and will help boost ASML’s revenue next year and beyond as chipmakers move to the latest technology to meet demand for AI chips. That, combined with the number of new fabs coming online in the coming years, bodes well for ASML’s long-term prospects.

At a previous analyst day, ASML management set a goal of growing revenues to €30 billion to €40 billion ($33.3 billion to $44.4 billion) by 2025 and €44 billion to €60 billion ($48.8 billion to $66.6 billion) by 2030. The company had revenues of €27.6 billion ($30.6 billion) last year and expects similar revenues this year.

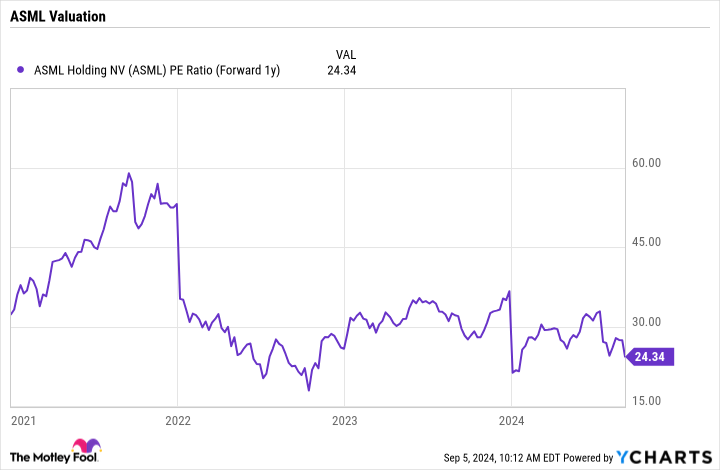

At a forward P/E of just over 24x analyst estimates for 2025, ASML stock looks attractive given its expected growth momentum going forward.

3. Arm holding

Am Holdings (NASDAQ: ARM) A leading semiconductor company for central processing units (CPUs), often described as the brains of a device, the company dominates the smartphone market, using this technology in almost every smartphone in the world.

Meanwhile, Arm is also targeting the personal computer (PC) market. The company’s technology is currently used in all apologize It sold computers and laptops, but its current goal is to capture 50% of Windows-based PCs in the next five years. It’s not as big a market as smartphones, but it’s still a good opportunity for the company. Arm has also made solid inroads in the automotive market. In Q2, it reported 28% year-over-year revenue growth in that segment.

Arm is also benefiting from AI. Last quarter, Arm said it had seen increased licensing in AI data centers because of the need for customization, and that it had partnered with Nvidia on a super chip that combines an Arm-based CPU with an Nvidia graphics processing unit (GPU). This technology is also the basis for CPU data center chips. Amazon and alphabet.

While semiconductor companies like Nvidia and Broadcom design their own chips, Arm uses a different model, licensing its technology to other companies so they can design their own chips based on it. Through licensing, it collects royalties on the shipment of chips that incorporate its technology. This revenue stream can last for years or even decades.

In recent years, the company has been moving its customers to a subscription model, allowing them to use its intellectual property more broadly. Through royalties or subscriptions, Arm has a largely recurring revenue stream with very high margins.

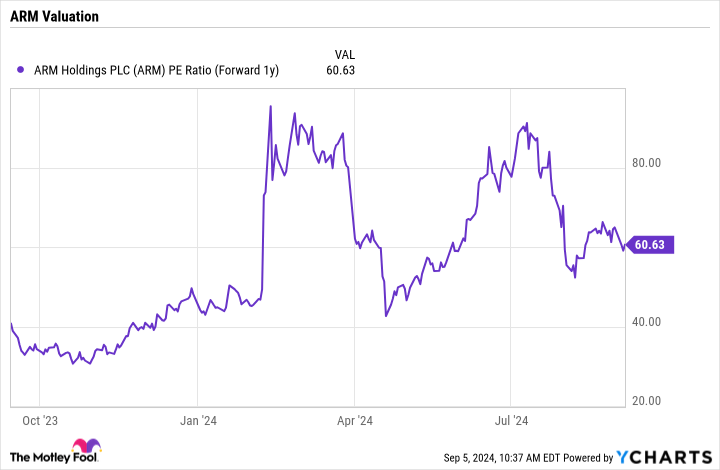

Arm stock trades at a forward P/E of just over 60.5x by analyst estimates for 2025. While that’s not cheap on the surface, it’s a downgrade from the top line, and Arm has one of the most attractive, long-tail business models in the semiconductor space.

Should you invest $1,000 in Arm Holdings right now?

Before buying Arm Holdings stock, consider the following:

that Motley Fool Stock Advisor The analyst team just confirmed what they believed. Top 10 Stocks Investors should buy now… and Arm Holdings wasn’t one of them. The 10 stocks that made the cut could deliver huge returns in the coming years.

When do you consider it? Nvidia We compiled this list on April 15, 2005… If you had invested $1,000 at the time of our recommendations, You will have $630,099!*

stock advisor It provides investors with an easy-to-follow blueprint for success, including guidance on portfolio construction, regular analyst updates, and two new stock recommendations each month. stock advisor There is a service Increased by more than 4 times The recovery of the S&P 500 since 2002*.

*Stock Advisor returns returns as of September 3, 2024.

Suzanne Frey, an Alphabet executive, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Jeffrey Saylor We have a position in Alphabet. The Motley Fool has positions and recommendations in ASML, Alphabet, Amazon, Apple, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and Intel and recommends the following options: Sell a November 2024 $24 call option on Intel. The Motley Fool has a position … Public Policy.

Buy Nvidia and 3 Other Stocks Amid Tech Selloff Originally published by The Motley Fool.

")