We have a lot of competitive assessments going on today, from the three Federal Reserve Banks and Goldman Sachs.

Figure 1: GDP (bold black), Professional Forecaster Survey August Interim Forecast (brown), GDPNow (blue squares), NY Fed (red triangles), St. Louis Fed (light green inverted triangles), Goldman Sachs (turquoise circles), all bn.Ch.2017$. Nowcasts are as of 9/6 except where noted. Nowcast levels are calculated by iterating the growth rate over the reported 2017Q2 2nd Release GDP levels. Source: BEA 2024Q2 2nd Release, Philadelphia Federal for SPFAtlanta Federal Reserve Bank (9/4), New York Federal Reserve Bank (9/6), St. Louis Federal Reserve Bank (9/6), Goldman Sachs (9/6), and author’s calculations.

furthermore, S&P Global Monthly Insights (formerly Macroeconomic Advisers) reported growth of 2.0% as of 9/3, slightly below GDPNow’s 2.1%.

The upward revision of Q2 GDP and the information that follows have resulted in nowcasts being uniformly higher than the SPF median forecast (reported in early August). It is difficult to see how much the short-term assessment of the likelihood of a recession has increased. For comparison, the SPF’s early August forecast probabilities are as follows:

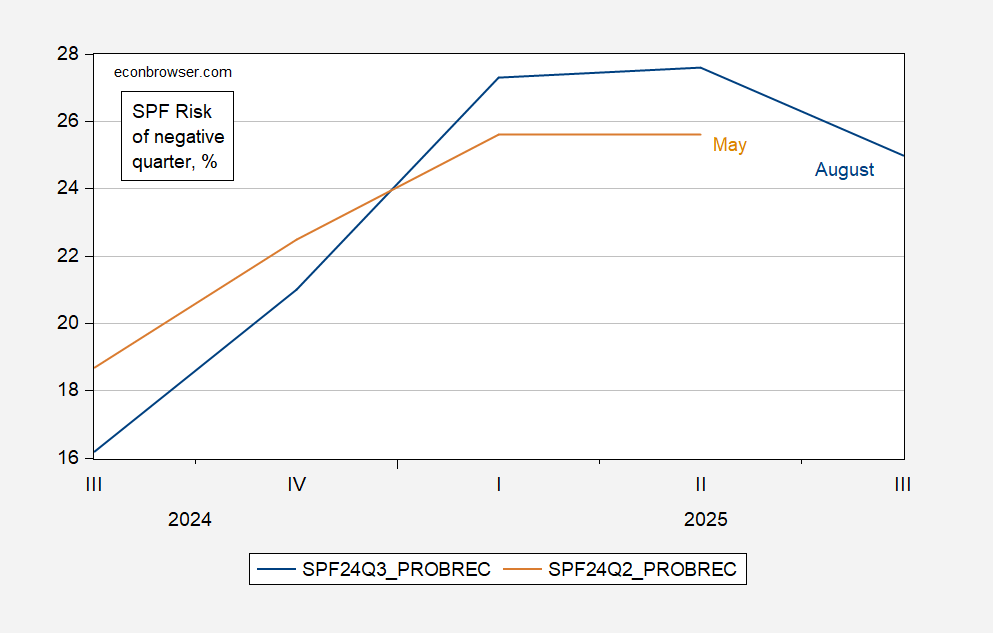

Figure 2: The risks of negative quarterly growth from the August survey (blue) and May survey (brown) are both %. Source: Federal Reserve Bank of Philadelphia.

The likelihood of a recession is lower in the near quarters (Q3, Q4) and higher in the distant quarters (Q1, Q2 2025).

: Vanraj’s shocking ultimatum to Meenu")