As previously observed, the explanation for why we do not yet see the onset of a recession in the data could be one of the following: (1) Models based on historical correlations are no longer applicable (DGP has changed), (2) we were using the wrong model. (3) The recession is not yet here, but it has not yet shown up in the data. Moreover, while the model may have been right, nothing is certain in the probabilistic world.

To summarize the predictions of the simple term spread model and the model including debt service ratio and foreign term spread:

Figure 1: ProBit with a simple period spread model estimated from 1986 to 2023M06 (blue), a model estimated from 1986 to 2018 (green) and a model with period spread, debt service ratio and foreign period spread estimated from 1986 to 2023M06. Recession probability forecast 12 months in advance (tan). Assume there is no recession as of November 2024. NBER defines recession dates as gray, from peak to trough. Red dotted line for 50% threshold. Source: NBER and author’s calculations.

It is interesting to note that the term diffusion model estimated for the entire sample, including the pandemic period, indicates a probability of more than 50% not only this month (December) but also several times in 2025.

There could be a recession in December 2024. Unfortunately, there is no data for December, nor is there any employment data for November yet. Nonetheless, as documented here, signs of a recession in October are not strong. Please keep in mind that all we have is preliminary data. (If that were the case, a recession would likely not have started in July 2024.)

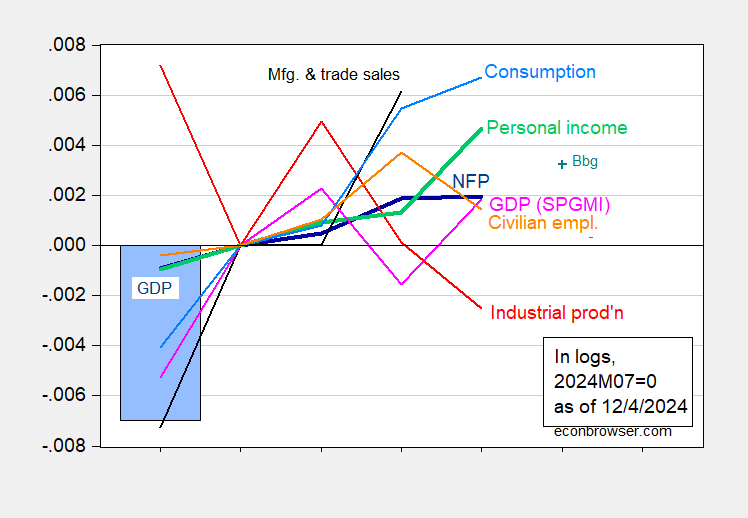

Figure 1: Nonfarm payroll (NFP) employment in CES (blue), Bloomberg consensus as of 12/4 (blue +), private employment (orange), industrial production (red), personal income excluding current transfers in 2017 Ch.2017$ (bold) light green) ), manufacturing and trade sales in Ch.2017$ (black), consumption in Ch.2017$ (light blue), Ch. Monthly GDP in 2017$ (pink), GDP (blue) bars), all logs normalized to 2021M11=0. Source: BLS, Federal Reserve, BEA 2024Q3 Second Release, via FRED; S&P Global Market Insights (nee Macroeconomic Advisors, IHS Markit) (12/2/2024 release) and author’s calculations.

On the other hand, it could be such a model. Chin and Ferrara (2024)Use foreign language spreads like this: Ahmed and Chin (JMCB, 2024) This could be a suitable model. Then you have little to worry about…

")